Early end to war may stabilize Korea’s economy in H2

Apr 16, 2026, 08:54 am

|

South Korea’s economy is expected to face a clear turning point depending on the trajectory of the Middle East conflict. If the war ends early, the country could regain growth momentum driven by semiconductor exports, with growth approaching 2%. However, a prolonged conflict raises the risk of stagflation, where economic slowdown and rising prices occur simultaneously.

Early End to War Could Restore Growth, But Inflation to Persist

If the conflict between the United States and Iran ends swiftly, South Korea’s economic growth this year is projected to come close to the government’s target of 2.0%. Strong semiconductor exports are expected to offset much of the shock from the conflict.

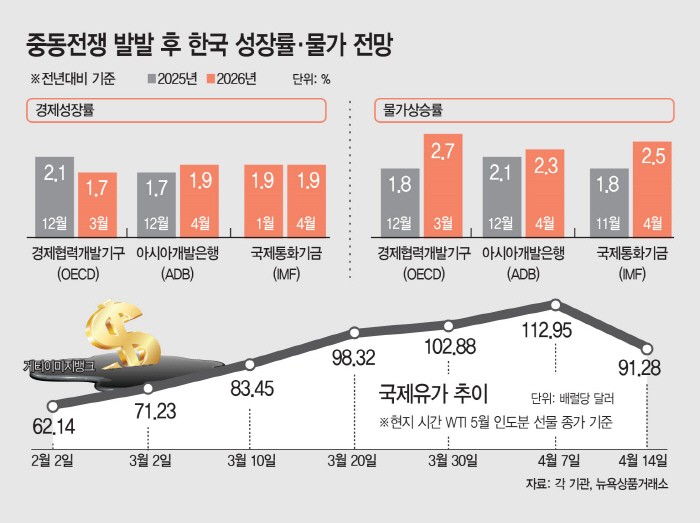

According to the Ministry of Economy and Finance on April 15, the International Monetary Fund (IMF) maintained its forecast for Korea’s growth at 1.9% in its April World Economic Outlook. The Asian Development Bank (ADB) also raised its forecast from 1.7% to 1.9%, aligning closely with the government’s earlier projection of 2.0%.

These forecasts are based on the assumption that the Middle East conflict stabilizes within weeks to about a month. With exports remaining resilient, an early resolution could place the Korean economy firmly on a recovery path.

Park Jin, a professor at KDI School of Public Policy and Management, said, “The Middle East conflict affects our economy through rising oil prices, reduced logistics flows, and weakened consumption due to financial market instability.” He added, “If negotiations lead to an early end, these issues could quickly return to normal,” noting that growth could normalize in the second half of the year.

However, inflationary pressure is expected to persist due to accumulated oil price shocks. The Korea Institute for International Economic Policy (KIEP) forecast that oil prices would remain around $90 per barrel even if the conflict ends early — about 43% higher than pre-war levels — citing the time needed to restore energy infrastructure.

High oil prices are likely to feed directly into domestic inflation. Unless energy prices drop sharply, cost pressures transmitted through producer prices will continue to affect consumer prices with a lag. Major institutions have already raised their inflation forecasts: the IMF to 2.5% (up 0.7 percentage points), the ADB to 2.3% (up 0.2 percentage points), and the OECD to 2.7% (up 0.9 percentage points).

Prolonged War Could Trigger Stagflation

If negotiations between the United States and Iran collapse and the conflict drags on, Korea’s economy could face a complex crisis, with simultaneous pressure on prices, financial markets, and the real economy.

The most immediate concern is a sharp rise in global oil prices. JPMorgan projected that if the Strait of Hormuz remains blocked until mid-May, oil prices could exceed $150 per barrel. Bloomberg Economics estimated that a three-month disruption in maritime transport could push prices up to $170 per barrel.

Additional risks in Middle Eastern shipping could drive up freight and insurance costs, further increasing the energy and logistics burden on companies beyond the rise in oil prices alone.

These cost shocks would spread quickly across industries via producer prices. Energy-intensive sectors such as refining, petrochemicals, transportation, and aviation would face soaring costs, leading companies to pass on these increases to consumers. This could push consumer inflation, currently in the low 2% range, into the 3% range.

JPMorgan warned, “If the Middle East situation does not materially improve, consumer inflation could exceed 3% between May and September, with high uncertainty thereafter.”

As these shocks accumulate, South Korea’s economic growth could fall to the low 1% range. This raises concerns that the country may enter a stagflation phase — a combination of high inflation and economic stagnation.

French investment bank Natixis projected that emerging Asian economies, including Korea, could face a stagflation environment beyond the control of central banks, lowering Korea’s growth forecast from 1.8% to 1.0%.

Professor Park also warned, “If the war is prolonged, we may face a recession along with supply-side inflation,” adding that “a scenario similar to the stagflation triggered by the oil shocks of the 1970s could re-emerge.”

#Korea economy #oil prices #inflation #Middle East war #IMF

Copyright by Asiatoday

Most Read

-

1

Katayama says, "No hesitation on further join..

-

2

Xi's loyalists to be at forefront of next leadersh..

-

3

Day after Russian sub leaves Cam Ranh, U.S. nuclea..

-

4

China's heatwave worsens, temperatures climb to 45..

-

5

New UK prime minister holds talks with Zelenskyy

-

6

U.S. military nearly exhausts long-range precision..

-

7

Man City topples Team K League without Haaland, Ro..

PEOPLE

-

Address : In-Young Bldg., 34, Uisadang-daero 1-gil, Yeongdeungpo-gu, Seoul

Copyright by ASIATODAY CO., LTD. All rights resereved