Samsung and Mirae launch high-stakes battle over leveraged chip ETFs

May 27, 2026, 08:25 am

|

Samsung Asset Management and Mirae Asset Global Investments are set to compete head-to-head in South Korea’s newly launched single-stock leveraged exchange-traded fund (ETF) market tied to Samsung Electronics and SK hynix.

The two asset managers will simultaneously list leveraged ETFs on May 27, with combined listing sizes exceeding 3.7 trillion won ($2.7 billion). Industry sources estimate that nearly 90,000 investors have already completed mandatory pre-investment education courses required for leveraged ETF trading.

The showdown marks the beginning of an intense competition between Korea’s largest asset managers over more than 200 trillion won in waiting capital in the domestic stock market.

Because the ETFs are tied to the same underlying stocks, analysts expect investors to compare products based on trading volume, bid-ask spreads and actual transaction costs stemming from creation and redemption structures.

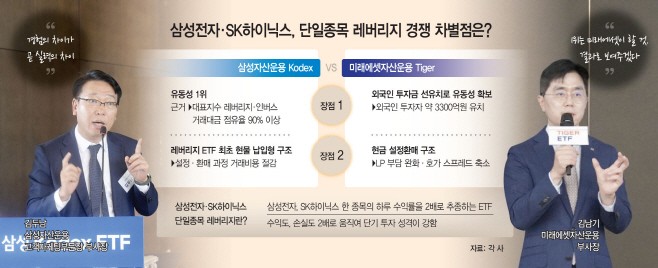

Samsung Asset Management highlighted its dominant market share in existing KODEX leveraged and inverse ETFs as well as its extensive liquidity provider (LP) network. Meanwhile, Mirae Asset emphasized its ability to attract approximately 329 billion won in foreign investor funds and its cash-based creation and redemption structure.

Both firms identified liquidity as their key competitive advantage, arguing that actual investor returns can differ depending on bid-ask spreads and market depth.

At separate press conferences on Monday, Samsung Asset Management unveiled the “KODEX Samsung Electronics Single Stock Leverage ETF” and “KODEX SK hynix Single Stock Leverage ETF,” while Mirae Asset introduced the “TIGER Samsung Electronics Single Stock Leverage ETF” and “TIGER SK hynix Single Stock Leverage ETF.”

Samsung Asset Management said it plans to expand the trading infrastructure already established in Korea’s leveraged ETF market into the new single-stock category.

“The company’s share of trading value in benchmark leveraged and inverse ETFs exceeds 90%,” said Lim Tae-hyuk, head of ETF management at Samsung Asset Management. “We currently work with around 21 liquidity providers in benchmark leveraged and inverse ETF markets.”

Samsung also emphasized that it introduced an “in-kind contribution” structure for leveraged ETFs for the first time.

Under the conventional cash-based structure, fund managers receive cash and directly purchase stocks and futures when creating ETFs, then sell holdings upon redemption. This process generates additional costs such as trading commissions and securities transaction taxes.

Under Samsung’s in-kind model, securities firms deliver stocks directly during ETF creation and receive stocks during redemption, reducing the need for the asset manager to trade physical shares.

Lim said the structure could reduce annual transaction costs by more than 1% compared with cash-based leveraged ETFs.

Samsung added that increasing the proportion of physical stock holdings could reduce futures rollover costs while allowing dividend income from underlying shares to flow into the fund.

Mirae Asset also stressed liquidity as its main strength but took a different approach, emphasizing the scale of foreign investor capital secured before listing.

Kim Nam-ki, head of ETFs at Mirae Asset, said the company had attracted 329 billion won from foreign investors for the two ETFs.

“We will demonstrate overwhelming liquidity through foreign investors’ active trading in single-stock leveraged ETFs,” Kim said.

Mirae Asset said the products were designed partly to redirect Korean investors who previously used overseas markets such as Hong Kong to trade leveraged products tied to Samsung Electronics and SK hynix.

The company also differentiated itself through its cash-based creation and redemption system.

In ETF markets, authorized participants (APs) and liquidity providers exchange assets with fund managers when creating or redeeming ETF shares. Under an in-kind structure, LPs must directly exchange stocks, potentially increasing transaction tax burdens that could widen bid-ask spreads.

Under a cash-based structure, however, LPs exchange cash instead of stocks, reducing the need to directly handle physical shares while using futures for hedging and market making.

Lee Jung-hwan, executive director of ETF management at Mirae Asset, said the system allows LPs to maintain tighter bid-ask spreads and more stable tracking errors without incurring stock transaction taxes.

Mirae Asset’s total listing size for the leveraged ETFs amounts to 1.3 trillion won — 747 billion won for SK hynix and 597 billion won for Samsung Electronics — compared with Samsung Asset Management’s 2.4 trillion won.

Responding to criticism over its relatively smaller fund size, Mirae Asset argued that sheer scale does not guarantee competitiveness.

“Once a fund reaches around 100 billion to 200 billion won, additional scale does not significantly improve quote competitiveness,” Kim said. “Excessively large funds can even create heavier rebalancing burdens.”

He added that fund structure, tighter spreads and lower tracking errors were more important factors.

“Mirae Asset has extensive experience in derivatives products. There is no reason not to choose us,” Kim said confidently.

Kim also expressed confidence about eventually overtaking Samsung in market share.

“In the past, our share in benchmark leveraged ETFs was not particularly high,” he said. “But these products are closer to semiconductor-themed and overseas investment demand than traditional index leveraged ETFs, so we believe we can become the market leader.”

#Samsung Asset Management #Mirae Asset Global Investments #Samsung Electronics #SK hynix #ETF

Copyright by Asiatoday

Most Read

-

1

Samsung Electro-Mechanics signs 300 billion won ML..

-

2

Pentagon reports roughly 100 U.S. troops injured i..

-

3

Trump says decision on large-scale attack on Iran..

-

4

South China on high alert as typhoon Noul expected..

-

5

New UK prime minister holds talks with Zelenskyy

-

6

Taiwanese President Lai Ching-te voices opposition..

-

7

U.S.-Iran armed clashes halt after two weeks, ente..

PEOPLE

-

Address : In-Young Bldg., 34, Uisadang-daero 1-gil, Yeongdeungpo-gu, Seoul

Copyright by ASIATODAY CO., LTD. All rights resereved