Market volatility and rising interest rates drive idle funds into top 5 banks

Jul 07, 2026, 10:18 am

|

| This image was generated by AI. |

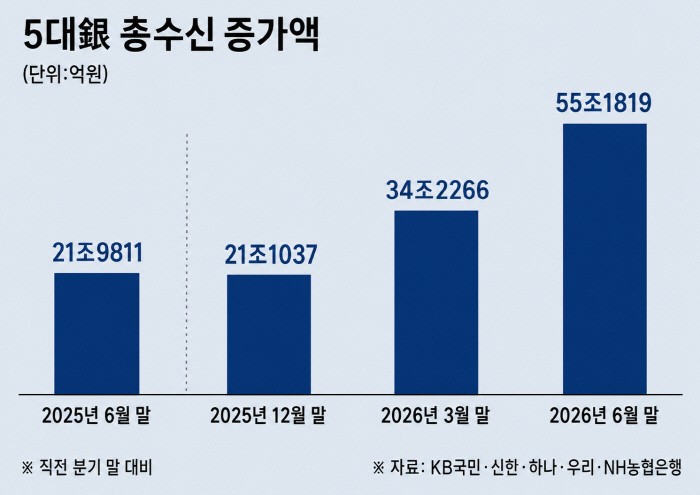

As the stock market undergoes violent swings and market interest rates continue their upward trajectory, idle funds from both investors and corporations are flooding into banks. Money that can be moved to alternative investment destinations at a moment's notice is staying in demand deposits, while funds seeking stable interest returns are resting in time deposits, leading both types of deposits to expand for the second consecutive month. This trend marks a reverse "money move," where a portion of the capital previously headed toward the capital markets is flowing back into banks amid heightened uncertainty. Consequently, the first-half growth in total deposits across the top five commercial banks expanded to nearly 1.9 times the level seen during the same period last year.

According to banking industry sources on July 6, the combined demand deposit balance of the top five banks—KB Kookmin, Shinhan, Hana, Woori, and NH Bank—stood at 722.2928 trillion won at the end of June, up 7.6351 trillion won from the previous month. This follows an 18.1052 trillion won surge in May, marking two consecutive months of growth and pushing the total balance to its highest level in four years. Because demand deposits allow depositors to withdraw funds whenever they choose, they are considered a primary vehicle for holding sideline cash when interest rates and asset market directions remain uncertain.

Capital is also pouring into time deposits. The top five banks' combined time deposit balance reached 949.3998 trillion won at the end of June, an increase of 4.6837 trillion won from the prior month. Given that balances rose by 7.5327 trillion won in May as well, the cumulative growth over the past two months has reached 12.2164 trillion won. Compared to the end of last year, the figure marks an expansion of 10.1135 trillion won.

The sustained rise in interest rates offered on deposit products appears to have driven the growth in time deposits. Data disclosed by the Korea Federation of Banks showed that the average maximum interest rate among 36 time deposit products offered across 18 banks stood at 3.16% per annum. Products offering a maximum rate of 3% or higher accounted for 58.3% of the total, numbering 21 products, while 13 products offered a base interest rate of 3% or higher even without preferential rate options. Analysts interpret that the increasing availability of products in the 3% range, moving alongside broader market rates, has attracted funds looking to lock in solid interest income.

"While total deposit levels can fluctuate from month to month based on the movement of end-of-month settlement and corporate funds," a banking sector official noted, "it is difficult to attribute the entire increase in demand deposits solely to retail investors taking profits from the stock market. However, it is clear that demand to secure liquidity has risen during this phase where stock prices and interest rates are moving in divergent directions."

The official added, "Considering that the expansion in total deposits during the first half of the year grew to a meaningful degree compared to the same period last year, and that both demand and time deposits expanded side by side, capital remaining within the banking sector is highly likely to continue shifting between secure deposits and risk assets."

Park Seo-ah

Most Read

-

1

Heung-min Son says "I'm sorry," but fans..

-

2

Iran’s IRGC attacks cargo ship in Strait of Hormuz..

-

3

Right-wing Fujimori wins Peru's presidential elect..

-

4

Japan invests 2 trillion yen in India to shift chi..

-

5

Khamenei's two-day funeral: Three sons spotted, su..

-

6

Netanyahu requests Trump to halt F-35 sales to Tur..

-

7

China codifies ‘One China’ policy as new ethnic un..

PEOPLE

-

Address : In-Young Bldg., 34, Uisadang-daero 1-gil, Yeongdeungpo-gu, Seoul

Copyright by ASIATODAY CO., LTD. All rights resereved