SK Ecoplant sees profit surge powered by chip boom, but keeping AI and semiconductor gains remains a task

May 18, 2026, 05:32 pm

|

SK Ecoplant recorded an "earning surprise" for the first quarter of this year, significantly beating market expectations and demonstrating the impact of its business reorganization centered on semiconductor and AI infrastructure. Along with top-line growth, a simultaneous shift in its revenue mix and raw material procurement structure led to a sharper improvement in profitability. However, some analysts suggest it is too early to interpret this earnings boost purely as a structural transformation of the company's fundamentals. With the semiconductor boom, the consolidation effect of subsidiaries, and pre-orders from certain business segments all contributing to the results, the key going forward remains whether the company can sustain its current level of profitability.

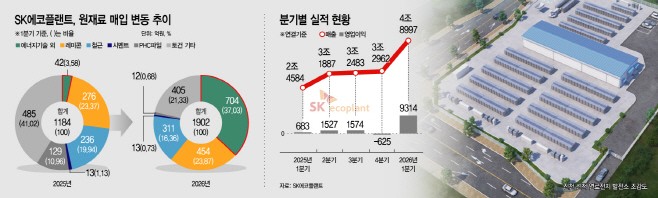

According to industry sources on May 18, SK Ecoplant's combined procurement share of traditional construction materials—including ready-mix concrete, rebar, cement, and PHC piles—stood at 41.6% in the first quarter of 2026. This marks a decrease of approximately 14 percentage points compared to the 55.4% recorded during the same period last year. Conversely, the share of energy technology materials surged from 3.6% to 37.0% over the same period, with the purchase volume of energy technology materials skyrocketing 16.5-fold from 4.2 billion won to 70.4 billion won.

This shift indicates that SK Ecoplant’s operational focus is moving from traditional housing, construction, and infrastructure toward the semiconductor, AI infrastructure, and energy technology sectors. The declining proportion of traditional construction material purchases is also interpreted as a factor that partially mitigates the company's exposure to cost volatility at construction sites.

This transition is particularly noteworthy given the growing cost burdens across the broader construction industry. SK Ecoplant's purchase price for ready-mix concrete rose from 91,400 won per cubic meter at the end of last year to 95,400 won in the first quarter of this year, while rebar prices increased from 894,000 won to 930,000 won per ton over the same period. Middle East geopolitical risks, maritime freight rates, and energy cost pressures are analyzed to have driven up overall raw material prices.

However, the reduction in traditional construction materials cannot immediately be equated with an improvement in cost competitiveness. This is because changes in procurement shares are influenced not only by cost-saving efforts but also by shifts in the revenue mix across business divisions and the consolidation of subsidiaries. In particular, given the sharp increase in energy technology materials, new cost variables—such as the procurement costs of high-value equipment and components, the securing of technical talent, and global supply chain risks—could intensify in the future.

The scale of the earnings improvement was substantial. In the first quarter of this year, consolidated revenue reached 4.8997 trillion won, a nearly 99% increase year-on-year. Gross profit expanded 5.5-fold from 204.9 billion won to 1.1311 trillion won, while operating profit skyrocketed 13.6-fold from 68.4 billion won to 931.4 billion won. This has led to assessments that the shift in the business portfolio has successfully translated into profitability rather than mere top-line expansion.

Performance by business segment also showed distinct changes. In the first quarter of last year, the largest revenue contributor was the Solution division—which encompasses housing, construction, infrastructure, and fuel cells—generating 973.3 billion won and accounting for 34% of the total. However, in the first quarter of this year, revenue from the Asset Lifecycle division—responsible for semiconductor reuse module manufacturing and distribution, electronic waste recycling, and ITAD services—surged to 2.3555 trillion won, making up 48% of total revenue.

Revenue from the Hi-Tech division, which handles semiconductor manufacturing facility construction and AI data center infrastructure development, also grew by 74.7% from 844.1 billion won to 1.4746 trillion won. Meanwhile, revenue from the Solution division dropped to 864.2 billion won. In essence, a profit structure once centered on traditional construction has rapidly shifted toward semiconductors, AI infrastructure, and resource circulation.

Nevertheless, whether this trend can be sustained requires further verification. The first quarter saw a concentration of pre-orders for raw materials related to the fuel cell business, which is utilized as a power source for AI data centers, alongside revenue mix adjustments from subsidiary consolidations. From the second quarter onward, as semiconductor factory construction accelerates, demand for traditional construction materials like ready-mix concrete and rebar could rise again. This implies that the expansion of the AI and semiconductor businesses cannot yet be viewed as a structural, permanent reduction in the share of traditional materials.

While the industry views these results as a clear signal that SK Ecoplant’s business transition is underway, it also believes the challenges ahead have become more defined. First, since revenues from semiconductor and AI infrastructure are highly sensitive to economic cycles and investment pacing, the company must manage the volatility that comes with an increased reliance on a specific industry. With the Asset Lifecycle and Hi-Tech divisions rising as primary drivers in a short period, securing a stable order backlog and recurring revenue streams is as crucial as maintaining profitability.

Cost management has also entered a new phase. While fluctuations in traditional construction materials like ready-mix concrete, rebar, and cement were previously the primary variables, profitability going forward will likely depend on energy technology equipment, semiconductor-related components, industrial gases, high-level technical talent, and global supply chain management capabilities. For the portfolio transition to move beyond a mere change in revenue mix and develop into sustainable earnings resilience, establishing a management system tailored to this new cost structure is seen as a core task.

An official from SK Ecoplant explained, "The first-quarter results reflect the transition of our business portfolio toward AI infrastructure and the performance of related businesses driven by the semiconductor boom. Each business division—including Hi-Tech, semiconductor materials and gases, Asset Lifecycle, and Solutions—is creating synergy as they reorganize around AI infrastructure and semiconductors." The official added, "Based on our capabilities in building semiconductor manufacturing facilities, our core task is to establish a business portfolio that spans across the entire AI infrastructure spectrum—including materials, industrial gases, and resource circulation management—thereby contributing to strengthening the competitiveness of the semiconductor industry ecosystem."

Most Read

-

1

Samsung Bioepis and PROTEINA partner to develop AI..

-

2

Iran's IRGC launches airstrikes on U.S. military f..

-

3

Trump imposes new Iran blockade and 20% Hormuz tol..

-

4

Netanyahu requests Trump to halt F-35 sales to Tur..

-

5

Khamenei's two-day funeral: Three sons spotted, su..

-

6

Samsung Electronics sets record with 89.4 trillion..

-

7

Chinese and Russian navies launch joint naval exer..

PEOPLE

HEADLINE NEWS

-

Address : In-Young Bldg., 34, Uisadang-daero 1-gil, Yeongdeungpo-gu, Seoul

Copyright by ASIATODAY CO., LTD. All rights resereved